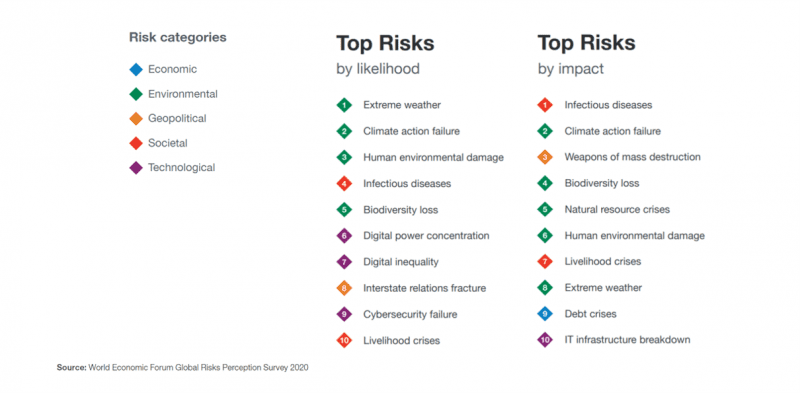

Environmental Threats Shape Risk Management in Insurance

In 2020, for the first time, the World Economic Forum in Davos (Switzerland) defined in its Global Risk Report 2020 that of the risks identified in this report, environmental risks are now considered significant global concerns. This forum brings together many world leaders who are committed to identifying major problems and risks to be addressed on the planet. These risks are categorized and represented by a color in the graphic below: Economic, Environmental, Geopolitical, Societal, and Technological, and have impact when thinking about risk management in insurance.

Unsurprisingly, one of the big changes between this year and last in terms of risks was brought about by the COVID-19 coronavirus pandemic. The risk posed by infectious disease is now ranked number one based on impact, up from number ten in 2020. More importantly, it has moved from a probability to a reality.

But despite the inevitable fallout from COVID-19, it is ‘climate-related’ issues that make up the bulk of this year’s risk list. The Global Risk Report 2021 describes it as “still an existential threat to humanity.”

The Global Risk Report 2021

Climate-related concerns

The reports above mention, “Governments, markets and, in an increasing number of societies, CEOs are awakening to the urgent realities of climate change—it is striking harder and more rapidly than many expected”.

The insurance industry is typically the first to be impacted by climate-related disasters, which result in huge financial losses, year-after-year, and continues to grow.

The cost of natural catastrophes in 2020 nearly doubled from the previous year, jumping from $116 billion to $210 billion, according to a report from global reinsurer Munich Re. Losses hit the U.S. particularly hard, totaling $95 billion, with damage primarily from hurricanes, storms, and wildfires.

In France, president of the French Insurance Federation declared in an interview with the magazine Risques, that “the average annual cost of climate-related losses has risen from €1.2 billion in the 1980s to €3.2 billion today and could reach €6.6 billion in twenty-five years.”

Climate risk is a central point of attention for all organizations. So, we immediately understand the importance of being able to evaluate risk. This is done with accurate and consistent data to make better informed decisions. In turn, estimating potential losses more accurately, leads to better predictions which provides more assurance for customers. New technologies also have their role to play in this global challenge.

Watch our Webcast

Delivering Efficiency and Customer Satisfaction to Claims and Underwriting with Dynamic Weather

Learn how carriers are taking advantage of more accurate and timely weather data while reducing the reliance on inefficient manual claims processes.

Predicting climate-related risks

Predictive climate risk analysis is powered by weather data, Artificial Intelligence (AI) algorithms, and location-based technology that links predictions to locations and assets. Companies in many industries are using geospatial intelligence to map and analyze information relevant to the locations in which they operate.

In climate change, domains like risk management, loss and exposure assessment, or parametric insurance have adopted new technologies for more sophisticated climate disaster prediction models. Advances in computational capabilities are the most obvious growth factor, with more data available, requiring accurate data. However, the models are evolving and need to be regularly recalibrated to avoid the phenomenon of BlackSwan, which corresponds to unmodeled losses. During a recent roundtable, in which Precisely participated, it was mentioned that including building footprints in the models will help better assess the financial impact of unprecedented weather events.

Gaining competitive advantage to better predict, prevent, and evaluate risk effectively has resulted in the “data race”. Whereby, more data sources are required, some static, others real time, in heterogeneous formats, ranging from Excel files from a broker to weather APIs. Spatial data, such as addresses or risk zones, are also to be considered, and must be as accurate as possible.

Operationalizing all this requires global data, tools, and more importantly, experts who are highly trained in this domain.

Precisely helps businesses by providing data to accelerate the insights required for risk management in insurance:

- A unique and persistent linkage, called PreciselyID, between millions of addresses and associated buildings and parcels, as well as thousands of data attributes to assist in the assessment of impact by climate threats.

- Detailed data on major risk factors such as earthquakes, forest fires, tornadoes, hurricanes, high winds, and other major weather events.

- Dynamic Weather data, which provides hyperlocal weather information for the past, present and future. Up to seven years of historical weather data allows for analysis of past losses, portfolio risk assessment, and increased pricing accuracy for new policies. Near real-time updates of current weather conditions allow insurers to be highly responsive, e.g., by sending out the First Notice of Loss (FNOL) notices. Forecasts help insurance companies take preventive measures to reduce risk (by informing customers of actions they can take, such as parking vehicles in a garage), or by pre-positioning adjusters in an affected area.

Monitor disturbances and adapt response

Another challenge is to become an insight-driven organization, at scale. Meaning maintain and organize operational data, which is current, automated, and available to separate areas in the insurance business.

For example, the provision of exposure reports, risk aggregations, or the supply of useful information for multiple user profiles (underwriters, brokers, marketing, legal, etc.) who are not data and mapping experts. However, they need to have access to relevant information which is adapted to their needs and in the simplest way possible.

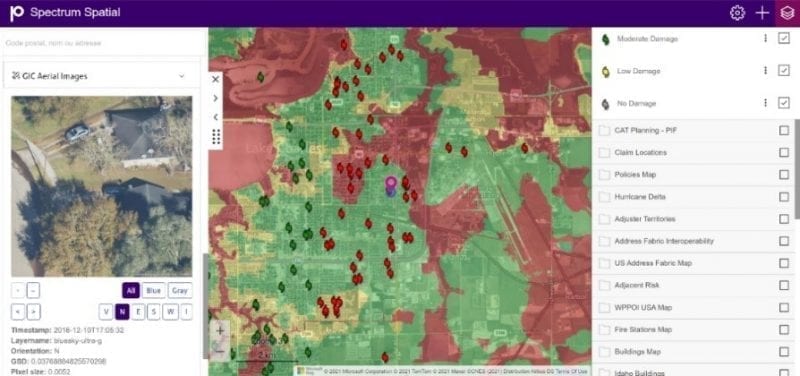

Organizations with data and technology have an advantage whereby executives and managers are duly informed and understand the issues. So, they can respond quickly, adjust, and make the right decisions. Spectrum Spatial addresses this challenge by providing a platform for centralizing and sharing information across the enterprise to the relevant stakeholders.

For example, a major risk team for a large French insurance organization integrated location intelligence with Spectrum Spatial into their operations. They can see the impact of a catastrophe on a portfolio by modelling the risks at a global level. Even better, they developed business modules, such as risk scores, on major global climate perils that allow the Risk Manager to easily interpret highly complex modelled risk data.

Building the future

The significant increase in climate impacts in 2021 underscores the urgency of adopting rapid and large-scale change for risk management in insurance. This must be supported by the digital technologies mentioned above such as, Location Intelligence and Geospatial data, and using technology and data we haven’t touch upon here like AI and satellite imagery.

Precisely helps democratize and industrialize spatial information across your organization, to deliver the real value and insights to you and your customers.

To learn how carriers are taking advantage of more accurate and timely weather data while reducing the reliance on inefficient manual claims processes, watch this webcast: Delivering Efficiency and Customer Satisfaction to Claims and Underwriting with Dynamic Weather

The Power of Location Data: Driving Business Value with Spatial Analytics

Key Takeaways Leverage location intelligence (LI) to make informed business decisions with spatial data insights. Use accessible LI tools to democratize data and enable competitive advantages. Ensure...

Location Intelligence Use Cases: Solving 5 Top Business Challenges

Key Takeaways: Harness the power of location intelligence to drive smarter, data-driven decisions that turn spatial data into a strategic asset. Top location intelligence use cases include efficient...

Ensure a Smarter Tomorrow by Unlocking Efficiency With Your Address Data Today

Virtually every business on the planet captures and stores address information. Ostensibly this data enables you to ship items or send mail to customers and prospects, to correspond with suppliers,...